By: Gabrielle Luoma CPA, CGMA

By: Gabrielle Luoma CPA, CGMA

In a previous post, we discussed who gets a 1099, and now you need to know how to fill out a 1099. Documents like this can be intimidating at first glance, but when you break them down it is quite simple. Here is our guide, box by box, of how to fill out a 1099.

How to fill out a 1099

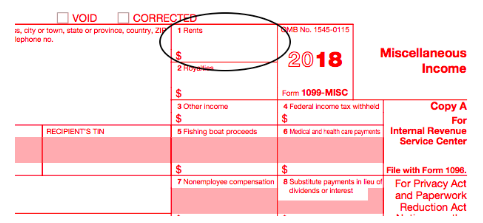

Box 1: Rentals

Examples of what goes in Box 1:

- Real estate rental for office space EXCEPT when paid to a real estate agent (the real estate agent will report to the owner)

- Machine rentals (example: a bulldozer)

- Pasture rentals

- Public housing agencies must report rental assistance payments made to owners of housing projects

- Coin-operated amusements if the arrangement between an owner of coin operated amusements and an owner of a business establishment where the amusements are placed is a lease of the amusements or amusement space

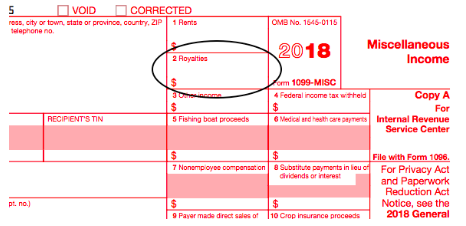

Box 2 Royalties:

Examples of what goes in Box 2:

- Gross royalty payments of $10 or more from oil, gas, or other mineral properties before reduction for severance and other taxes that may have been filed

- Royalty payments from intangible property such as patents, copyrights, trade names, and trademarks

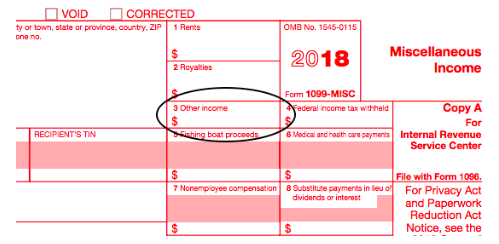

Box 3 Other Income:

Examples of what goes in Box 3:

- Report other income if $600 or more

- Awards and prizes that are NOT for services performed

- Indian gaming profits, payments to tribal members

- Payments to individuals for participating in medical research study(ies)

- Termination payments to former self-employed insurance salespeople

- All punitive damages, any damages for nonphysical injuries or sickness, and any other taxable damages

- Foreign agricultural workers

*The lines can overlap between Boxes 3 and 7. IRS has guidelines to determine what should be reported in each box. If unsure, research and confirm all criteria that differentiates which box to report said income.

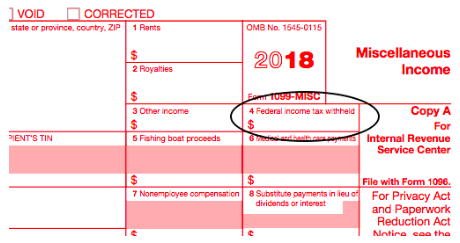

Box 4 Federal Income Tax Withheld:

Examples of what goes in Box 4:

- Backup withholding for persons who have not furnished their TINs are subject to withholding on payments required to be reported

- **See part N in the General Instructions for Certain Information Returns

- **Income tax withheld from payments to members of Indian tribes from the net revenues of class II or class III gaming activities conducted or licensed by the tribes

Box 7 Non-Employment Compensation:

For box 7, Non-employee compensation of $600 or more with the following conditions:

- You made the payment to someone who is not your employee

- The payment is for services in the course of your trade or business (including government agencies and nonprofit organizations)

- Your payment is to an individual, partnership, estate, or, in some cases, a corporation. These payments to the payee must be of at least $600 during the year

- Professional service fees, such as fees to attorneys (including corporations), accountants, architects, contractors, engineers, etc

- Fees paid by one professional to another, such as fee-splitting or referral fees

- Payments by attorneys to witnesses or experts in legal adjudication

- Commissions paid to non-employee salespersons that are subject to re-payment but not repaid during the calendar year

Box 6 Medical and Healthcare Payments

Examples of what goes into Box 6 (payments of $600 or more):

- Any physician or other supplier/provider of medical or health care services

- Include payments made by medical and health care insurers insurers under health, accident and sickness insurance programs

Box 13: Excess Golden Parachute Payments

- Enter any excess golden parachute payments. This is any excess over the base amount of the average annual compensation for services included in the individual’s gross income over the most recent 5 tax years.

Box 14: Gross Proceeds to an Attorney

This box is for the Gross Proceeds Paid to an Attorney. Enter gross proceeds of $600 or more paid to an attorney in connection with legal services (regardless of whether the services are performed for the payer). For more information, see Payments to attorneys in the section for Box 7.

Have more questions?

We would love to help you more with your 1099 or other tax needs. Contact us for more information about how our services can help ease your worries as you close out this fiscal year.

**Note that the form included in this blog post is meant for information only. For more details about this notice, please visit: https://www.irs.gov/pub/irs-pdf/f1099msc.pdf

You May Also Love

CLOSE